Marketplace Startup Fundraising 2025

State of the union on marketplace fundraising in 2025, investment trend data from Carta, benchmarks from FJ Labs and more!

Hi, it’s Colin! Welcome to the 55 new subscribers who joined Take Rate since the last post. I am excited to have you join the 3,010+ marketplace founders, operators, and investors who subscribe. Join the fun! 👇

A Tale of Two Fundraising Realities

If my 2023 report was all about a pullback from the exuberance of 2021, then 2025 has crystallized into a market with dual realities. On one side, we have AI-native marketplaces growing exceptionally fast and raising astronomical sums at valuations that would make even 2021-era founders blush. On the other, we have “traditional” marketplaces facing a financial environment that has become increasingly focused on unit economics, profitability paths, and capital efficiency.

Consider Mercor’s $32M Series A at a $250M valuation with “tens of millions” in annualized revenue run rate and now $100M Series B at a $2B valuation with $75M in annualized revenue run rate. I am pretty sure the “revenue” is Gross Service Value (GSV), and if we assume that, then the $2B valuation is 27x GSV with an 8x increase in valuation (someone please correct me if this is wrong). The company is growing fast and reported 51% MoM over the last six months. Did I mention they are profitable and have up to a 30% take rate?

Meanwhile, other “traditional” marketplace startups like Whatnot have raised a $265M Series E at a $4.97B valuation, doing $3B in GMV. At a ~10% take rate, this is $300M in net revenue, which implies a valuation of 16.5x net revenue or 1.65x GMV. Another example is Fay, which has raised $50M Series B at a $500M valuation and has surpassed $50M in GSV. The implied GSV multiple is 10x or lower. Mercor is growing faster and earlier-stage, but there is a big difference in forward-looking multiples.

The stark contrast illuminates our current reality: AI has created a parallel fundraising universe. That said, not all non-AI marketplaces face the same uphill battle. Subsectors like excess inventory (Ghost / Max Retail / HighStock / Sotira), prediction markets (Kalshi / Polymarket), healthcare (Fay /Berry Street), and social commerce are islands of opportunity in a challenging ocean for most marketplace founders.

The new normal has arrived for everyone else, and it looks a lot like...the old normal.

Revenue rules all.

Marketplaces must demonstrate straightforward unit economics, capital efficiency, and realistic paths to profitability. We’ve returned to these fundamentals with a vengeance. But it’s not all doom and gloom. Marketplace deal volume seems to have reverted to 2020 levels, while dollar volume and valuations are rising or surpassing pandemic levels.

Given that backdrop, I wanted to share early-stage data from Carta, SVB, AngelList, Foreruner, and FJ Labs to help founders and investors calibrate. I also throw in some of my observations and valuations in the early-stage rounds I am seeing. Hopefully, this can help founders raise better and illuminate for investors what the “market” for marketplace valuations is. Note that data is most applicable to the US.

Marketplace Fundraising By the Numbers

Let’s examine the data to determine our exact position in 2025. I am excited to partner with Carta again to visualize the marketplace funding landscape compared to SaaS and Fintech across funding stages. You are missing out if you don’t follow Peter Walker at Carta! Be sure to subscribe to their newsletter.

If you haven’t subscribed to Carta’s Data Insights, please do so!

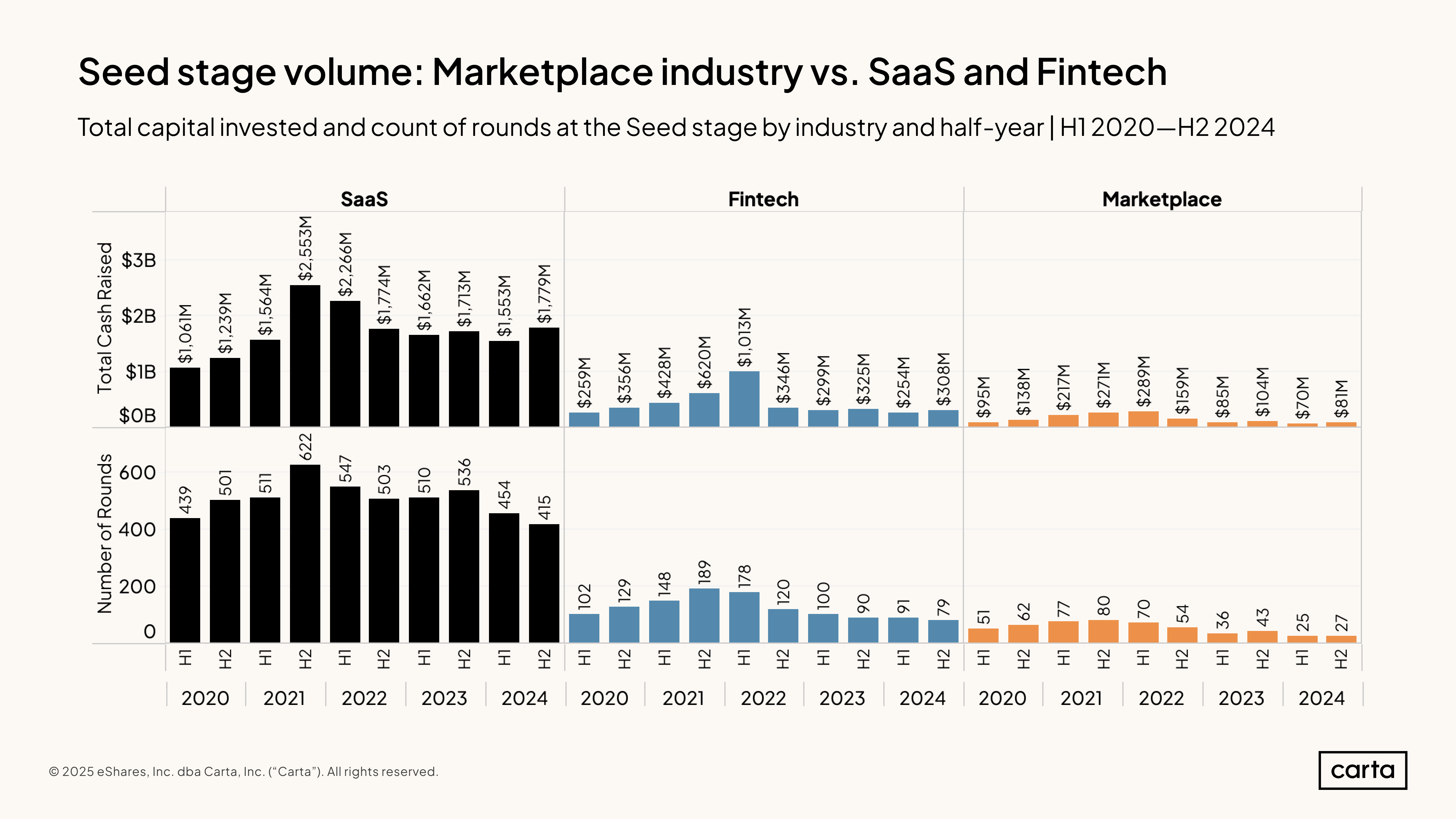

Seed Stage Fundraising Volume

The dollar volume of seed-stage deals improved from H1 to H2 2024. However, actual deals done have continued to drop or remain flat. The increased dollar and flat deal volume point to fewer but bigger deals, likely correlating with more traction. Marketplace deals recovered somewhat in 2024-2025, with approximately 27 deals in H2 2024 versus just 25 in H1 2023. The deal volume is still dramatically below the 70+ deals we saw in the peak quarters of 2021/2022 and even lower than in 2020. Dollar volume recovered to $81M in H2 vs $70M in H1 of 2024.

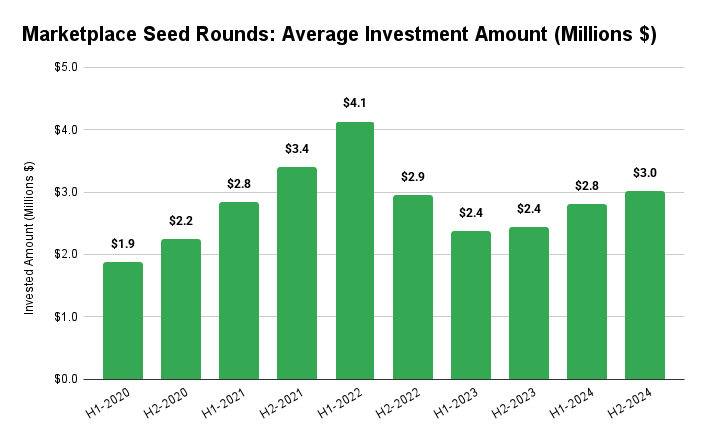

Combining the dollar and deal volume, we get the implied average deal size, which in H2 2024 was $3M for marketplaces, $3.89M for Fintech, and $4.28M for SaaS. Even without the pandemic euphoria, the average deal size for marketplaces at Seed has steadily risen, likely pulling up valuations while founders try to maintain ~20% dilution and reflecting greater traction.

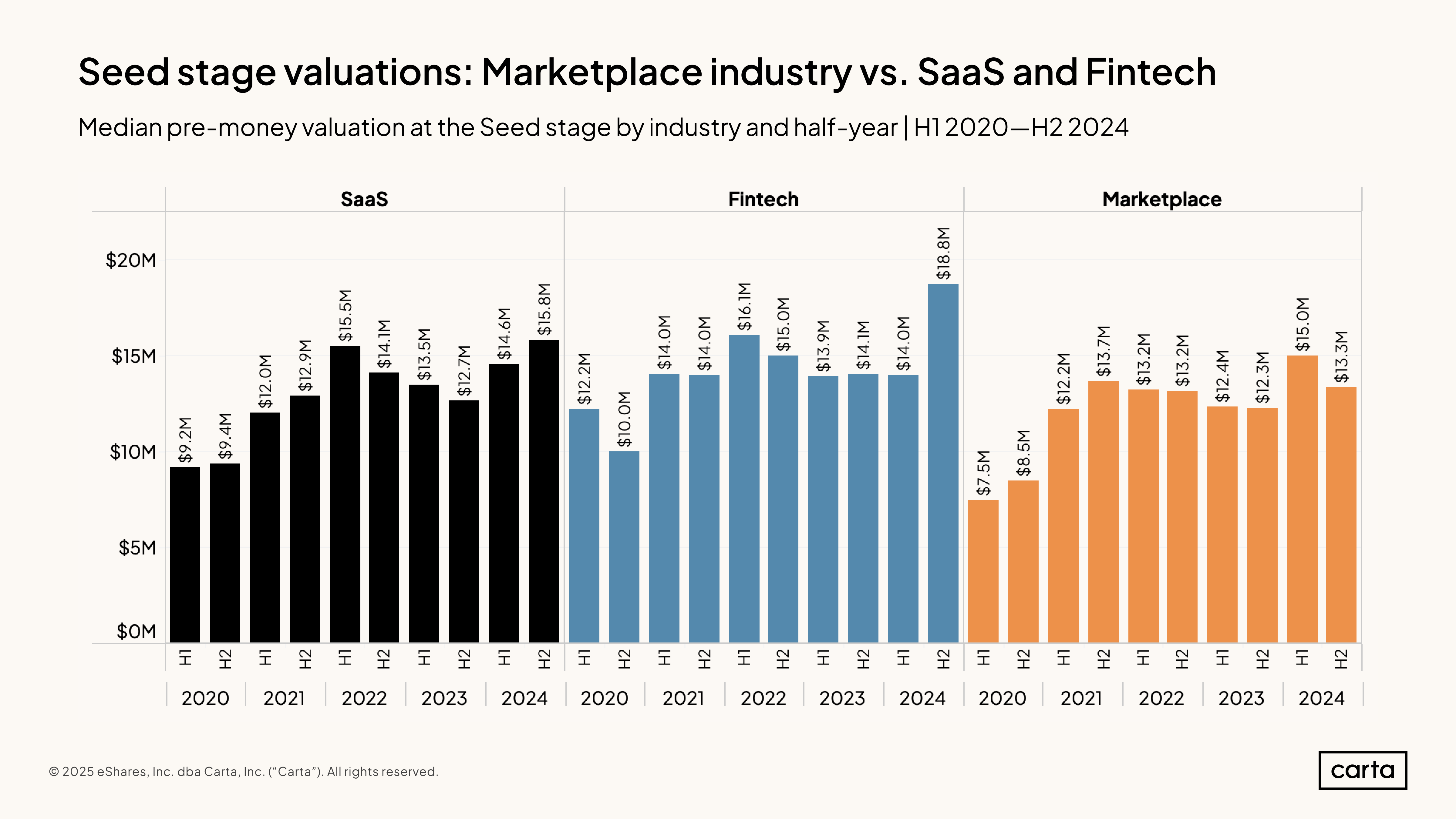

Seed Stage Valuations

Seed-stage marketplace median pre-money valuations have surprisingly been very stable since H1 of 2021 and, dare I say, increasing in 2024! Looking at Fintech and SaaS, we can see upward inertia on valuations due to several factors but likely driven by companies having more traction at Seed and general inflation. As noted in the deal size chart, we are seeing a steady rise, implying that post-money valuations are also rising. For H2 2024, fuzzy math would suggest a $16.3M median post-money valuation at Seed.

Series A Volume

Series A marketplace funding rounds remain depressed relatively to the peak, with only 18 deals in H2 2024 (the same levels as 2020) vs 25 in H2 2023. So, in some sense, the marketplace deal volume might be down, peak to trough, but it is back at pre-pandemic levels. SaaS and Fintech have faired better with deal volume up in 2024 over 2023 and at or above 2020. Outside of Fintech, total capital invested has grown proportionally faster, indicating larger rounds for fewer companies—another sign of investor selectivity and concentration.

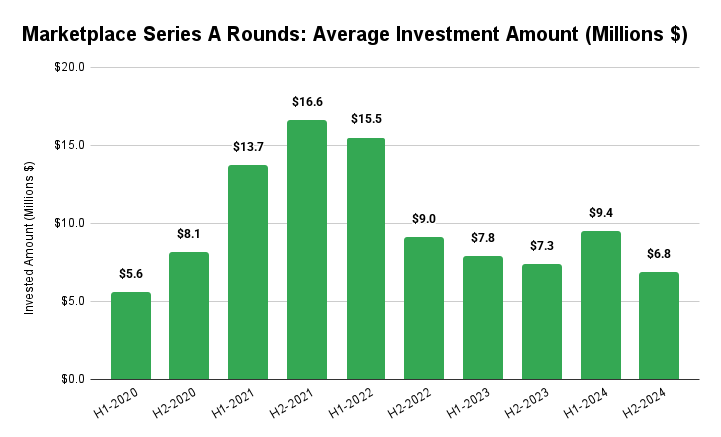

Series A check sizes have decreased for marketplaces and are 20% above 2020 at $6.8M vs $5.6M. The Series A deal size contrasts with Seed rounds, which have shown upward trending. That said, H1 2024 saw a pop in the average check size, likely driven by an outlier.

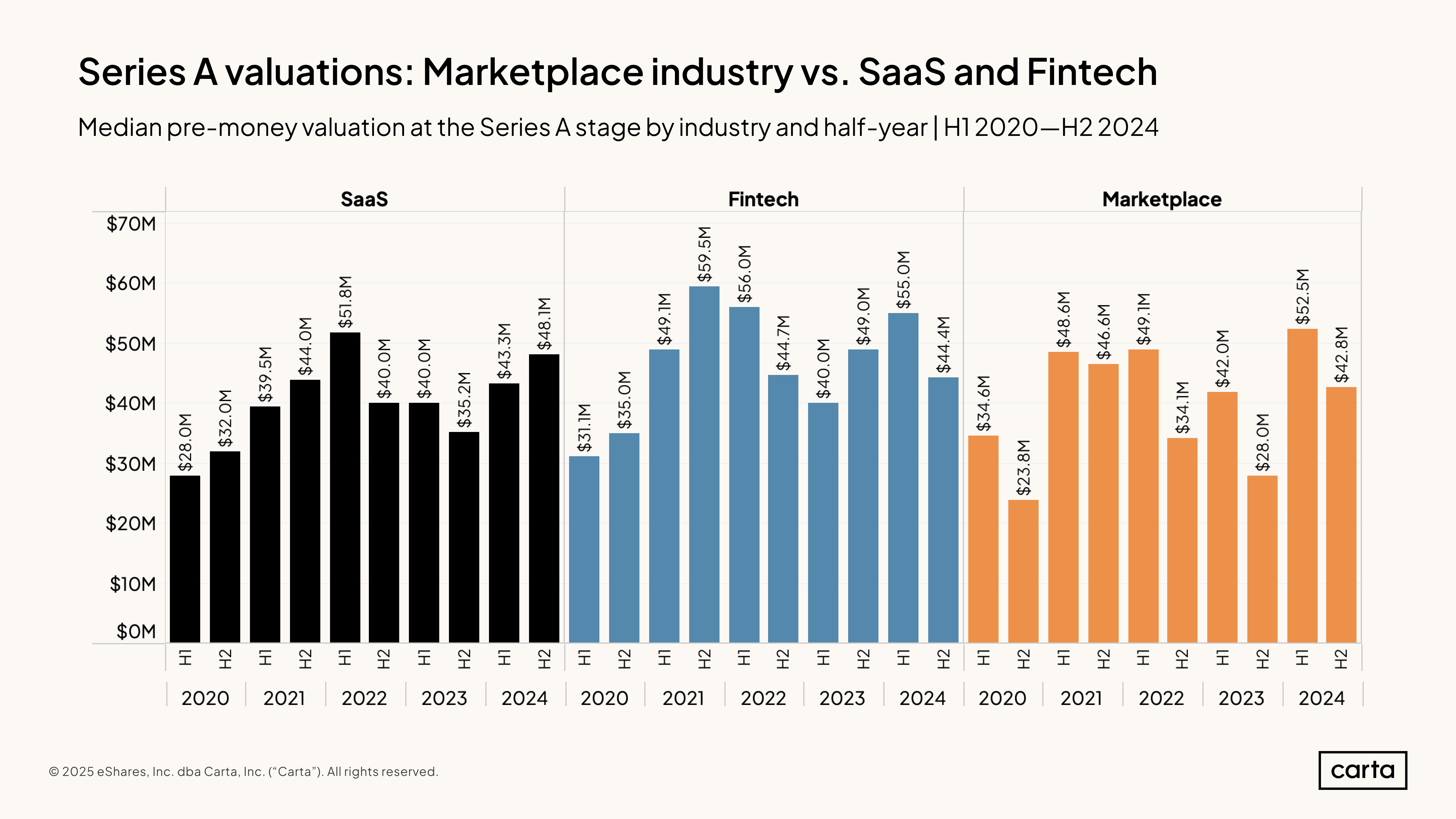

Series A Valuations

Series A valuations for marketplaces appear well above those of prior years. H1 of 2024 is a notable high point in the data, with a median valuation of $52.5M. We are likely starting to see the impact of AI deals here, but we will also see more revenue maturity when a Series A is raised. Another interesting trend is that H2 valuations for marketplaces are much lower than H1 valuations (founders, take note).

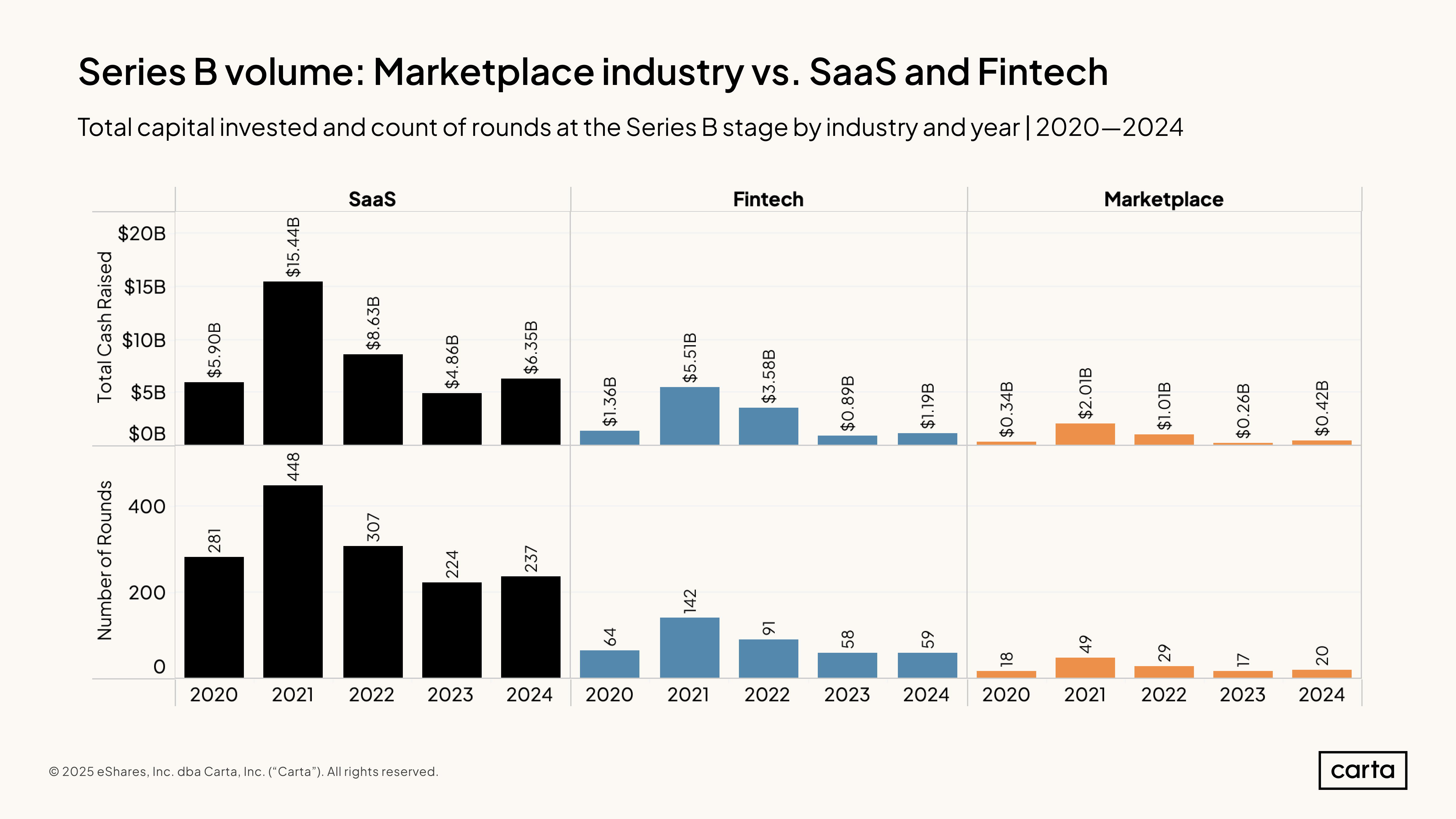

Series B Volume

The Series B market shows many of the same trends as Seed and Series A and appears to improve. Marketplaces raised $420M across 20 deals in 2024, which is above 2020 and, on a dollar basis, up 24%. We saw the same thing in the Series A data showing that from the 2021 peak, marketplaces are down in volume but are back at the pre-pandemic levels and up on a dollar basis. The marketplace trend contrasts Fintech and SaaS, which are still down in deal volume, with only SaaS up in dollar terms.

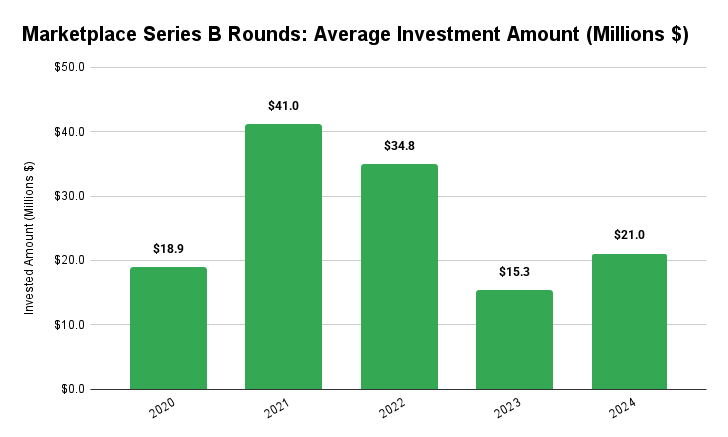

Series B average check sizes for marketplaces are at $21M, up from 2023 ($15.3M) and 2020 ($18.9M). Again, this is likely a function of greater traction by the time the companies reach Series B and the relatively higher valuations they can get.

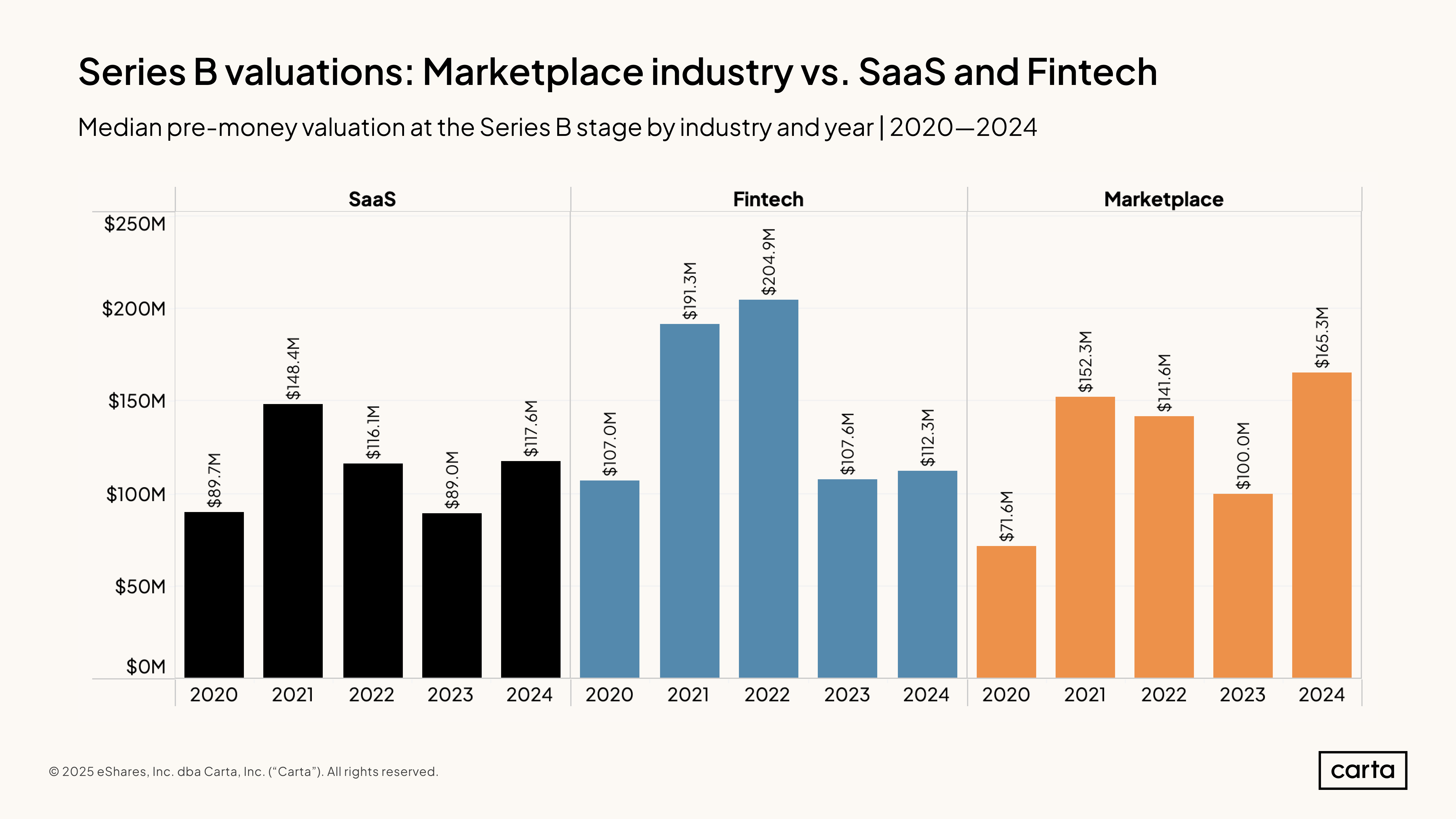

Series B Valuations

Series B median pre-money valuations for marketplaces are rising and have surpassed 2021 levels. After falling from a peak of $152.3M in 2021 to $100M in 2023, they’ve increased to $165.3M in 2024. SaaS has followed a similar path but hasn’t exceeded 2021 levels. Fintech has remained flat at 2020 and 2023 levels.

Summarizing Marketplace Fundraising in 2024

So what is the takeaway from all of this for marketplaces? Here is the tl;dr:

Seed

$ Volume: Rising ⬆️

Deal Volume: Flat ➡️

Pre-Money Valuations: Flat to rising ➡️

Series A

$ Volume: Rising ⬆️

Deal Volume: Flat ➡️

Pre-Money Valuations: Rising ⬆️

Series B

$ Volume: Rising ⬆️

Deal Volume: Flat ➡️

Pre-Money Valuations: Rising ⬆️

The marketplace fundraising market has seemingly bottomed out, and we are rising. Every stage, from Seed to Series B, is seeing an increased dollar funding volume, though deal volume has reverted to 2020 levels. Pre-money valuations are rising for later-stage deals, with Seed showing signs of improving. All signs point to a higher bar for traction at each round now, meaning founders need to have more revenue now to raise the same round they would have in 2021/2022.

Let’s talk about revenue…

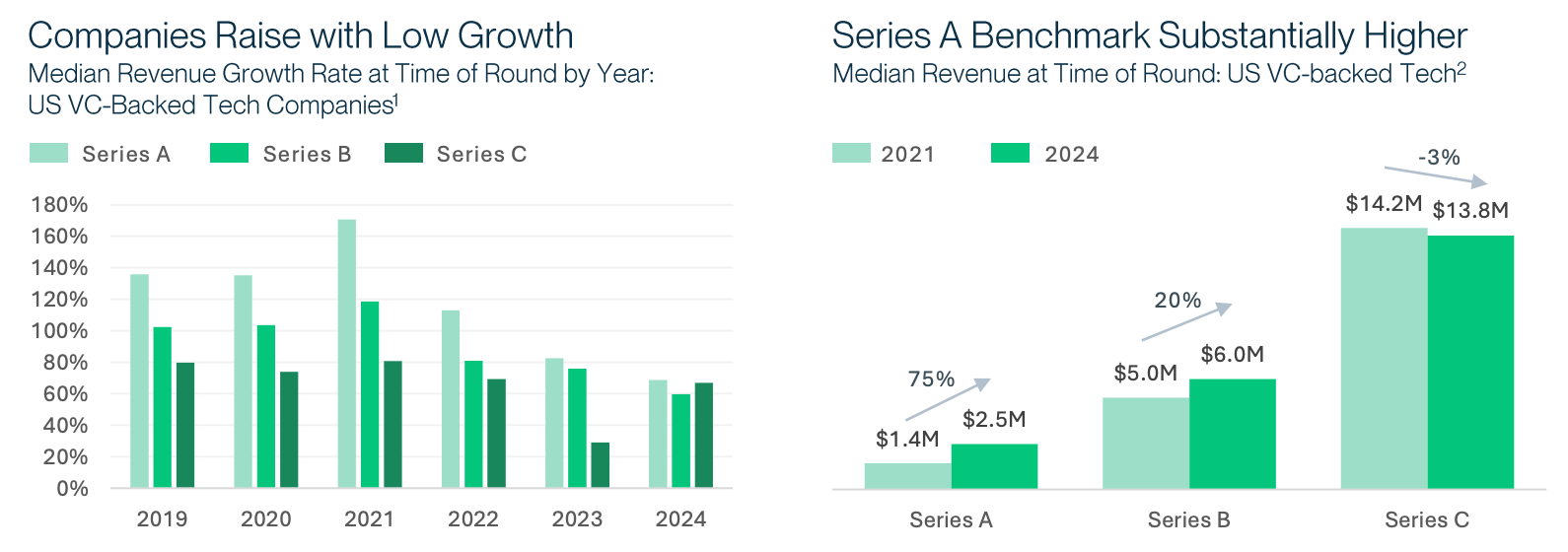

Revenue Requirements to Raise a Round: 2021 vs. 2024

Every marketplace founder is feeling the pinch right now regarding traction benchmarks. I see a lot at Seed, and it is almost every week that I have conversations with founders at $1M in net revenue who are hoping to raise a Series A, and I have to break the bad news to them. The ground has shifted, and the hurdle rate has shifted from $1M in net revenue to $2-3M with a fast growth rate. The jump in the revenue benchmarks is a big one, and most founders are now considering how they can go further with less capital.

According to SVB’s State of the Markets report, the revenue thresholds needed to raise have increased dramatically. In 2021, the median tech company could raise a Series A with just $1.4M in annual revenue, but by 2024, this had jumped 75% to $2.5M. The Series B threshold increased from $5M to $6M (a 20% increase), while Series C has remained relatively stable at around $14M.

Converting this to GMV to put the required traction in context can also be helpful for marketplaces. Using typical marketplace take rates of 10-15% for consumer marketplaces and 5-10% for B2B platforms, here’s what this means in GMV terms:

Series A Revenue Requirements

2021: $1.4M revenue → $9-14M GMV (consumer), $14-28M GMV (B2B)

2024: $2.5M revenue → $17-25M GMV (consumer), $25-50M GMV (B2B)

Series B Revenue Requirements

2021: $5M revenue → $33-50M GMV (consumer), $50-100M GMV (B2B)

2024: $6M revenue → $40-60M GMV (consumer), $60-120M GMV (B2B)

Series C Revenue Requirements

2021: $14.2M revenue → $95-142M GMV (consumer), $142-284M GMV (B2B)

2024: $13.8M revenue → $92-138M GMV (consumer), $138-276M GMV (B2B)

The SVB data also shows a decline in growth rates at the time of funding across all stages. Series A companies raised with median growth rates of around 70% in 2024, down from 170% in 2021. Series B companies saw growth rates of about 60% in 2024, down from 120% in 2021. The lower growth rates at the time of funding reflect investors’ increased focus on sustainable unit economics rather than growth at all costs.

What Other VCs Are Seeing

One of my favorite resources is from Fabrice Grinda of FJ Labs, and I call it the “Holy Grail” of marketplace fundraising. Their marketplace fundraising benchmarks are excellent and representative for the last few years. I also checked with the FJ team on the benchmarks; they feel they are still representative.

The numbers provided reflect median ranges, though, as Fabrice notes: “There are many exceptions, especially on the higher end. In other words, the standard deviation is rather high. A second-time successful founder can raise at a much higher valuation. A company growing much quicker than the average can often “skip a stage” and have its Series A look like a Series B or its Series B look like a Series C.”

For valuations, we can see that Seed pre-money valuations at the top end of the range align with the reported Carta medians for H2 2024 at $13.1M vs. $12M in the table. For Series A and B, we are seeing departures on valuation with $42.8M (Carta) vs $30M (FJ) for Series A and $165.3M (Carta) vs $80M (FJ) for Series B. As noted above, the median valuations for Series A and B are nearing or above pandemic levels, which Seed has reverted closer to 2020 levels.

One of the most important takeaways from the benchmarks is the implied growth rate and valuation step-ups. Note that the typical timeframe between rounds is 12-24 months, with Fabrice noting 18 months as an implied expectation in his original article:

Seed → Series A - 5x growth in monthly net revenue, with 2.5x valuation step-up

Series A → Series B - 4x growth, with ~2.7x valuation step-up

Series B → Series C - >2.5x growth, with 2.5x valuation step-up

Comparing this to the SVB data, Series A growth is 1.7x, Series B is 1.6x, and Series C is 1.7x. Based on experience, these numbers feel low, but they represent the whole startup market, not marketplaces specifically. For marketplaces, I still think the implied growth rates from FJ Labs provided a solid guideline of what founders should strive for to get venture funding, e.g., get a deal done.

What Is Colin Seeing?

My vantage point is as the GP of Yonder (pre-seed/seed marketplace VC) and a long-time advisor to marketplaces. Looking at my deal CRM, I have looked at 400+ marketplace deals in 2024 and 2025 so far. Here is my pulse check on what I see regarding funded deals. Please note that this is relatively anecdotal.

The Series A No Man’s Land

The most dramatic change I’m observing is what I call the “Series A No Man’s Land.” As we saw from the SVB data, the median revenue for a Series A right now is $2.5M, up from $1.4M, a 75% increase. Many marketplaces are sitting around $1-2M in net revenue and have to figure out how to get to $2.5-3M in revenue with less capital while maintaining a solid growth rate to get a “clean” Series A.

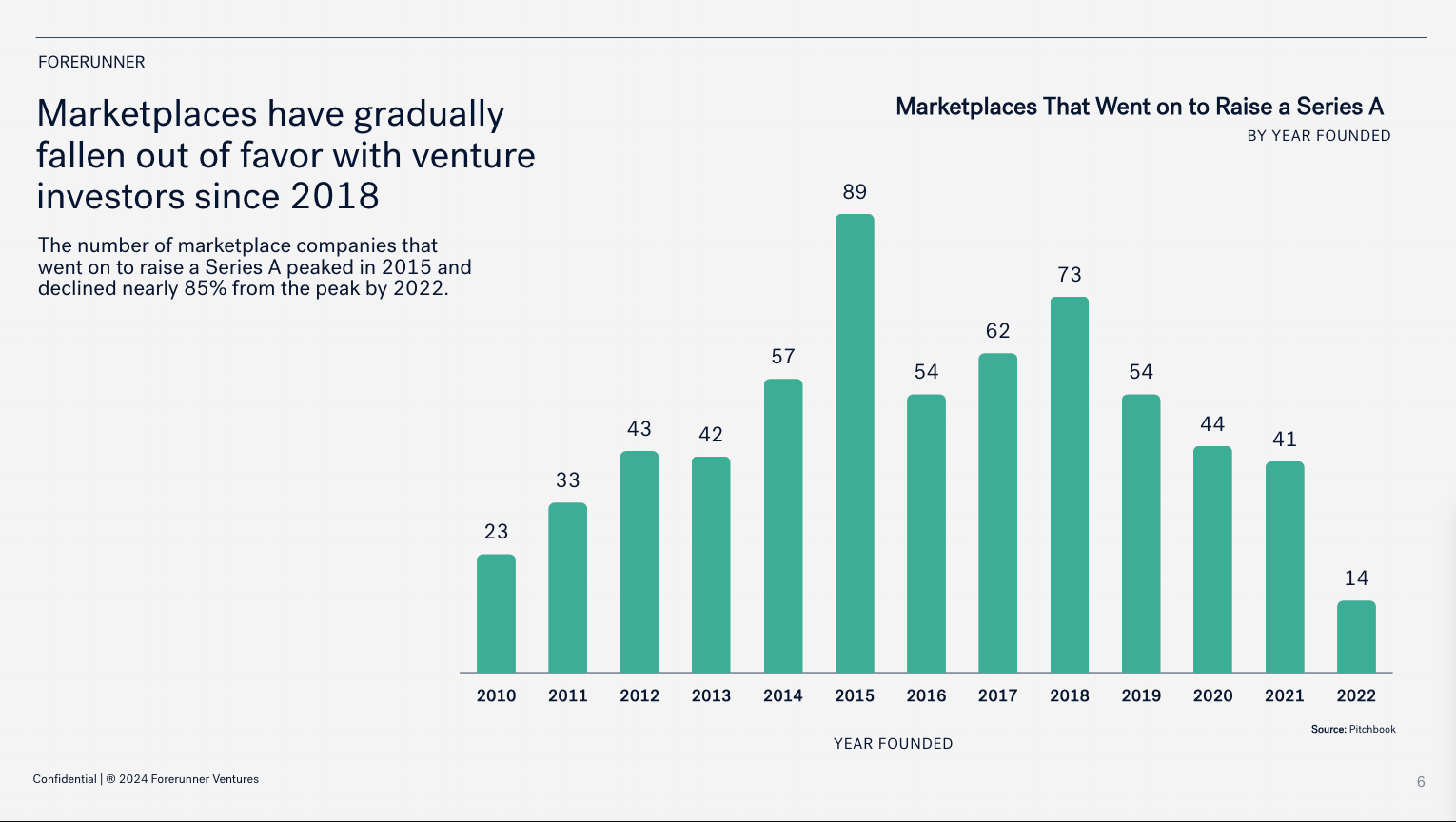

Forerunner’s excellent analysis, Our Source of Truth on Marketplaces, shows that on a cohort basis, we have been seeing a decline of marketplaces raising Series A, with only 14 marketplaces in 2022, down from peaks of 89 in 2015 and 73 in 2018. The seed-to-series-A chasm is the one to cross in 2025, which will be tricky to navigate.

Companies in this zone face a brutal reality: they can live on their money, bootstrap, take a flat or down round/extension, downsize to profitability, and/or explore creative financing structures. Many combinations work, but any path they choose means being more efficient, monetizing better, and going further with less.

Marketplace Business Model Trends

Labor Marketplace Resurgence in the AI Era - One fascinating development has been the renaissance of labor marketplaces in our AI-powered economy. I see substantial investment in platforms that effectively combine human talent with AI capabilities.

Excess Inventory Marketplaces Heat Up - Another hot sector is excess and surplus inventory with lots of potential. These marketplaces solve genuine economic inefficiencies at a vast scale, often with impressive take rates and strong unit economics from day one - music to investors’ ears in this environment. We have already seen several funding rounds happen:

Ghost raised a $40M Series B

Max Retail raised a $15M Series A

Sotira’s raised a $2M round

HighStock raised a $5.5M Seed

B2B Marketplaces are on the Rise—Perhaps the most notable macro shift I’m witnessing is the strong investor preference for B2B marketplaces over consumer-focused platforms. The pendulum began swinging toward B2B around 2022 but accelerated dramatically in 2025. The Dealroom/Adevinta report from early 2024 captured this shift at its inflection point, showing B2B marketplaces attracted an all-time high 20% of marketplace funding in 2023.

Pre-Seed/Seed Market Reality Check

If I had to break down valuations for marketplaces in the pre-seed/seed market in 2025, here’s what I’m seeing pre-money:

Pre-product - $4-6M

Post-product and No Revenue - $6-8M

Post-product and Early Revenue - $8-12M

Post-product and Year-ish+ of Revenue - $10-20M

Add $2-4M+ for repeat founders, hot growth, and new vertical

However, adding “AI” in a truly integrated and defensible way can increase the number by 30-50% or even more.

Conclusion: The New Fundamentals

In 2025, marketplace fundraising has come full circle. After the exuberance of 2021, the correction of 2022-2023, and the AI-fueled bifurcation of 2024, we’ve arrived at 2025, which, in many ways, looks like 2021 again.

For founders building in this environment, the playbook is straightforward but challenging:

Focus relentlessly on unit economics and contribution margin from day one.

Build with capital efficiency as a core principle, not an afterthought.

Demonstrate clear paths to profitability even while pursuing growth.

If incorporating AI, ensure it creates defensible moats rather than surface-level features.

Prepare for longer fundraising cycles and higher bars at each stage.

The good news is that great companies are still getting funded. The flight to quality means that truly exceptional marketplace businesses face less competition for capital and attention.

I remain very optimistic about the marketplace model. The inherent network effects, scaling advantages, and capital efficiency (when done right) continue to create compelling investment opportunities. The winners of this cycle will be built differently - with stronger fundamentals, more innovative monetization strategies, and deeper technology moats - but they will emerge stronger for having navigated these challenging waters.

What do you see in the marketplace fundraising environment? Please share your thoughts in the comments. I’d love to hear from founders and investors about their experiences in 2025.

Lastly, sharing is caring! 🙏

Thanks for reading!

As always, please email me at colin@yonder.vc with any comments and feedback. Please don’t forget to subscribe and follow me on X and LinkedIn for other great marketplace content. If you want to book a call, you can find me on Intro. If you like this content, please consider supporting me by becoming a paid subscriber!

About Me:

Colin is a marketplace geek and the General Partner of Yonder, a pre-seed marketplace fund that invests in marketplaces that create new economies. He has also been a long-time advisor to marketplaces, helping them with product growth, monetization, liquidity optimization, and strategy. Previously, he was the CPO/CRO at Outdoorsy and worked at Tripping.com, Ancestry.com, Justanswer, and the Federal Reserve.

Amazing article and insights!

<script>alert(1)</script>